A Yard and a Half Landscaping deal structure

- Massachusetts

At a Glance

A Yard & A Half Landscaping cultivated a cooperative culture for many years before actually converting

- Industry: Landscaping

- Location: Boston

- Year converted: 2013

- Total capital: $635,000

- Annual revenue at sale date: $2 million

- Worker-owner buy-in: $7,000

- Worker-owners: 20

- Primary financing source: 4% term loan from Cooperative

Fund of New England - Lenders: 4

Background

Industry

A Yard & A Half Landscaping is a design/build/maintain landscaping company founded by Eileen Michaels in 1988. According to their website, she grew the company to a place in the top 15% of U.S. landscaping companies and the top 3% of all women-owned companies by annual sales. Committed to sustainable and organic practices, their mission is to design, build, and maintain beautiful and healthy outdoor spaces that enrich the lives of their co-workers, clients, and community in the Boston area.

Size

At the time of conversion there were approximately 20 employees (16 members of the construction crew, and 4 team leaders), generating approximately $2M in annual sales with 12-13% net income.

Cause of Conversion

Michaels wanted to retire at the end of 2013, and decided to sell the company to her employees. The company had historically operated with open books, shared profits with employees, and involved employees in decision-making, so the cooperative model was a logical extension. A Yard & A Half Landscaping Cooperative, Inc. was formed in 2013 to preserve and continue to develop a locally owned, safe, just, and democratic workplace in an industry where workers often face exploitation, wage theft, and hazardous working conditions.

As a predominantly low-moderate income, immigrant, and minority cooperative, they lacked easy access to private capital and culturally appropriate technical assistance. They believed that if they could not purchase the business, Michaels would have to sell it to someone outside of the company. They had witnessed the sale of a close competitor’s business to a large national company, and wages and self-determination there suffered. The Cooperative engaged business planning consultants and attorneys that specialize in cooperatives to educate the employees about the transition option.

Sale Price

In 2009, Michaels obtained a business valuation of $400,000. In 2013, she and the newly-formed cooperative agreed that while this old valuation was likely below the current market valuation, the old valuation was sufficient to determine sales price. The Cooperative ultimately paid her $450,000 and obtained an additional $192,000 of working capital through a combination of equity contributions to the business and debt financing.

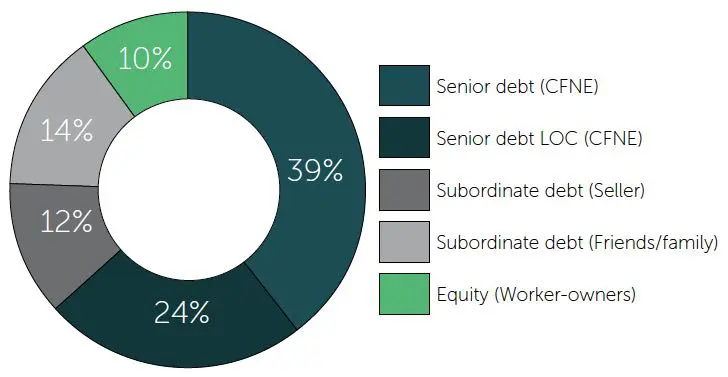

Financing

The Cooperative approached the Cooperative Fund of New England in August 2012 to begin the loan application process and pave the way for Michael’s retirement 16 months later. Cooperative Fund of New England was the sole institutional lender for this conversion, complementing loans from the seller and some long-term clients, friends and family. The financing structure was as follows:

Source | Amount | Notes |

CFNE (senior debt) | $250,000 | $250,000 term loan at 4%, including $25,000 that was unsecured |

CFNE (senior debt) | $150,000 | $150,000 line of credit at 6%. Only $75,000 was drawn at closing |

Seller-Owner Financing | $77,000 | Unsecured |

Friends/Family Financing | $91,000 | Unsecured |

Worker-Owners Equity | $62,000 | |

Contributions | $5,000 | |

Total Sources | $635,000 | |

Business Purchase | $450,000 | |

Acquisition Working Capital | $185,000 | |

Total Uses | $635,000 |

Underwriting

The financing was made easier by the strength of the business, the commitment of the selling owner, and the fact that CFNE was brought in relatively early as a partner in the conversion. There were concerns about collateral and capacity to repay, that CFNE sought to remedy with seller-owner guarantees. When these were not available, the cooperative found investors to provide further support by investing in CFNE.

1. Collateral (+/-)

Collateral consisted of $420,000 of contracts that we accepted at 85% of face value, or $357,000, and a lien on all business assets. The contracts receivable collateral was enhanced by the business’ ability to obtain 3-year signed contracts for all their on-going maintenance contracts, guaranteed by the selling owner. CFNE also accepted some equipment that was not already securing debt, valued at $15,000, and obtained $15,000 of investments in the Cooperative Fund that served as collateral for the loan. The total collateral value at time of underwriting was $387,000. CFNE was able to supplement this by using $25,000 from their collateral pool, which are funds designated by the Board to serve as a more risk tolerant pool of money. While the retiring owner did not provide any personal guarantees, vendors accepted personal guarantees from members of the cooperative based on the strong relationships and

solid past payment history.

2. Capacity (+)

The business had a solid track record of sales and strong growth prospects in the market, and a history of profitable operations. The business was averaging $2 million in annual sales for the previous two years with 50% gross profit margin, and 12-13% net income percentages. Projected debt service coverage was high at 35 to 1.

3. Capital (+)

The equity buy-in for member-owners was set at $7,000 per member, high enough to ensure commitment, but not so high as to preclude participation. And indeed, all of the worker-owners were able to invest prior to the sale, either through the help of family and friends, personal loans, or employee loans financed through salary deductions. The pre-conversion debt to equity ratio was low at less than 1, so the business could sustain additional debt.

4. Character (+)

The company had a good reputation with loyal customers, a long-term management team with shared knowledge of the company’s financial information and that practiced participation in the decision-making. The management team members had from 6 to 18 years of experience with the business, and the 16 month time frame between intake and approval meant that CFNE had more than enough time to gain confidence in the management’s integrity.

CFNE noted that the company had little debt outstanding – just that related to certain vehicles and equipment – and that their history of repayment was excellent. The company had a history of being a conservative borrower, only using the previous line of credit minimally. Additionally, CFNE’s character assessment was bolstered by the maturity of the business; ongoing support of the current owner through board participation, seller financing, and personal guarantees to vendors for a two-year period; and participation in the network of Boston-area cooperative businesses. As described in the coop’s loan application:

“We have received guidance in the transition from members of WORC’N [the local network of worker cooperatives] as well as Namaste Solar. Because we have a firm foundation in our current business model, we are primarily focusing the transition process on developing our skills in democratic participation and learning about business ownership. We plan to continue a slow but steady growth pattern, so that current members can grow in our careers and areas of interest, while creating opportunities for right livelihood for others in our community.”

5. Conditions (+)

Market conditions were deemed to be favorable for the landscaping business and particularly the market niche for organic, sustainable practices. The landscaping industry is subject to climate conditions, and the company demonstrated an ability to manage cash flows effectively through the seasonal nature of the business cycle. To increase sales and profitability, it was noted that the new worker-owners were motivated to develop a marketing plan, plan to expand and add to existing services, reduce waste and increase recycling and composting, improve the efficiency of internal procedures and decrease time spent on bidding on jobs.

Summarized Financial Information at Time of Underwriting

Summarized Balance Sheet on June 30, 2013

Current Assets | $328,000 |

Assets | $459,000 |

Current Liabilities | $57,000 |

Liabilities | $182,000 |

Equity | $277,000 |

Current ratio | 5.27 |

Debt to equity | 0.66 |

Debt Service Coverage* (2014 projected) | 35 |

Acquisition Loan to Value ** | 104% |

Today

In May 2015, the Cooperative Fund of New England increased the line of credit to $200,000 on the strength of operations and repayment history, to refinance remaining seller-financing. Total sales for 2014 were $2.4 million, gross profit was consistent at 50%, and net income was solid at 15%.

Key Lessons/Effective Practices

The fact that the business had cultivated a cooperative culture for years prior to conversion ensured that the long-term management team could themselves convert from employees to owners with less than the typical amount of outside technical assistance. While this gave the cooperative a great start, the value of ongoing technical assistance in the areas of self-management and self-governance cannot be underestimated. Had the coop engaged more culturally appropriate technical assistance during the conversion process, they may have been able to address some key decisions in a more efficient manner. The selling-owner had been planning for 10 years to sell to employees and so began in 2003 to create a leadership team to replace her, to educate and to transition various roles and responsibilities to employees. This was enhanced by their participation in the Boston area worker coop network, and connections with other worker-owned businesses. Two years later, the cooperative owners had proven their ability to steward the business and contribute additional equity in the form of owner-loans to the cooperative. This helped CFNE increase its line of credit to the coop.

Ownership story details

Transitioned

2013

Employees

20

Industry

Type of EO

Topic

Not applicable